When India’s Union Cabinet amended its foreign direct investment (FDI) policy on March 10, 2026, introducing a 60-day expedited approval window for Chinese industrial investment in seven manufacturing sectors, the move was widely interpreted as another sign of improving India–China relations following the 2020 Galwan Valley crisis. However, the amendment reflects industrial necessity more than political normalization.

For six years, India sought to reduce Chinese influence in strategic sectors through tighter investment scrutiny, visa restrictions, and domestic manufacturing mandates. Despite these measures, dependence on Chinese technology, machinery, and upstream industrial inputs remained largely intact. In several sectors, restrictions delayed capacity creation without generating viable alternatives.

The March 2026 amendment therefore reflects a broader recognition that supply-chain resilience cannot be achieved through restrictions alone. Where domestic capabilities remain underdeveloped, limiting foreign participation can constrain industrial growth rather than reduce dependence. The sectors covered by the revised framework—electronic components, capital goods, polysilicon and ingot-wafer manufacturing, advanced battery components, rare-earth processing and permanent magnets—share a common characteristic: China occupies a dominant position across their global supply chains. India’s selective reopening to Chinese capital is thus an attempt to reconcile strategic caution with industrial reality.

The Origins of India’s Supply-Chain Nationalism

The 2020 measures were not simply a reaction to the Galwan clash; they built on an earlier, broader anxiety about economic dependence and ownership concentration in strategic sectors. Press Note 3 (PN3), issued on April 17, 2020, predated Galwan and required prior government approval for investments from countries sharing a land border with India, representing an effort to prevent opportunistic takeovers during the Covid downturn.

Such concerns had been accumulating for years. Since 2014, Chinese capital and commercial presence in India expanded beyond infrastructure into technology startups, digital platforms, and advanced manufacturing, prompting worries in New Delhi about strategic exposure and concentrated foreign ownership. At the same time, the Atmanirbhar Bharat program, launched in May 2020, consolidated an industrial‑policy turn toward domestic manufacturing and technological self‑reliance. Solar manufacturing occupied a prominent place within this vision. Even before PN3, India had begun using trade and industrial-policy instruments to protect domestic producers, including safeguard duties and later Basic Customs Duties on imported solar cells and modules.

However, policymakers likely underestimated the degree to which India’s manufacturing ambitions were dependent on Chinese industrial ecosystems. Firms seeking rapid scale repeatedly relied on Chinese machinery, intermediate components, and on‑site technical support, particularly in solar PV, electronics and advanced batteries.

The Post-Galwan Policy: Expanded Restrictions

The Galwan Valley clash in June 2020 transformed what had begun as a precautionary investment-screening mechanism into a broader framework of economic restriction. While the objective was to reduce strategic vulnerabilities arising from dependence on China, the measures that followed produced consequences that extended beyond investment flows and increasingly impacted wider industrial development.

For example, following the deterioration in India-China relations after Galwan, India sharply curtailed the issuance of Chinese business visas. Annual visa approvals reportedly fell from approximately 200,000 in 2019 to approximately 2,000 by 2024, a 99 percent reduction. While intended as a security measure, the restrictions exposed the fact that many of India’s emerging manufacturing sectors remained dependent on Chinese technical expertise. Manufacturers awarded production-linked incentive (PLI) allocations in solar PV, advanced chemistry cell batteries, and electronics frequently relied on Chinese equipment suppliers for installation, calibration, and commissioning. Critical machinery such as ingot-growing furnaces, wafer-processing systems, and precision manufacturing equipment often required specialized engineers from the original equipment manufacturer, so visa delays disrupted project timelines and slowed capacity expansion.

Another set of measures focused on procurement and trade policy. Instruments such as the Approved List of Models and Manufacturers (ALMM), together with safeguard duties and later Basic Customs Duties on imported solar cells and modules, sought to stimulate domestic manufacturing by creating a protected market for Indian producers. Critically, however, these policies did little to address the upstream capability constraints that continued to limit domestic production.

The cumulative effect became visible across multiple sectors. The India Cellular and Electronics Association estimated that visa restrictions and related operational bottlenecks contributed to approximately USD $15 billion in lost production opportunities in the electronics sector between 2020 and 2023, alongside nearly 100,000 forgone jobs.

The Galwan Valley clash in June 2020 transformed what had begun as a precautionary investment-screening mechanism into a broader framework of economic restriction.

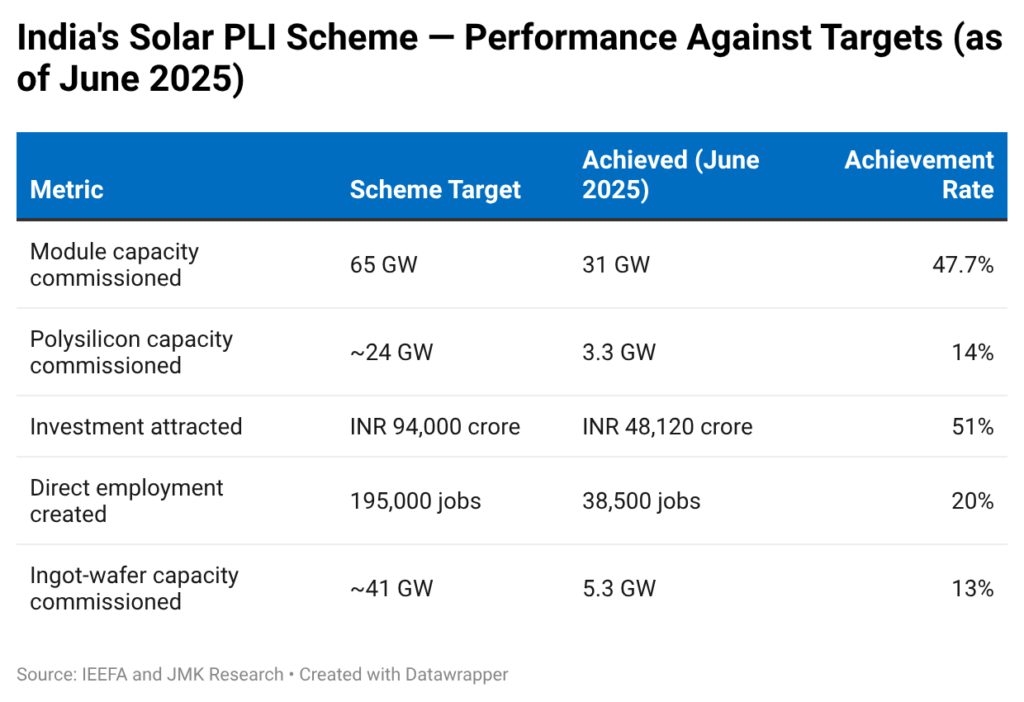

Nowhere was the gap between policy ambition and industrial capability more evident than in the solar PLI scheme. Designed to create an integrated domestic manufacturing ecosystem, the program succeeded in expanding downstream module production, but achieved only limited progress in upstream segments. As of June 2025, India’s module manufacturing capacity had reached 120 GW, while polysilicon capacity stood at only 3.3 GW—a striking 36 to 1 ratio that underscored the continued weakness of the country’s upstream supply chain.

Supply Chain Realities: China’s Structural Dominance

The relative inefficacy of these policies can in large part be attributed to Chinese dominance over critical supply chains in the energy, technology, and manufacturing sectors. China’s sweeping control is most visible in the upstream segments of the solar value chain. For instance, in 2024, China accounted for 93.5 percent of global polysilicon production, with nine of the world’s ten largest producers located in the country. Chinese producers also account for more than 97 percent of global ingot and wafer production, giving them control over the critical upstream stages that determine costs and competitiveness across the broader solar manufacturing ecosystem.

In fact, China’s influence extends well beyond solar PV and increasingly shapes the wider clean-energy industrial landscape. The country accounts for approximately 91 percent of global rare earth refining and 94 percent of sintered permanent magnet production both of which are critical for electric vehicle motors, wind turbines, advanced electronics, and defense systems. Chinese firms also account for 53 percent of global battery material export trade and hold dominant positions, at 80 percent or above, across most midstream battery supply chain segments.

India’s position within these supply chains remains comparatively limited. As of June 2025, the country possessed approximately 3.3 GW of polysilicon capacity and 5.3 GW of ingot-wafer capacity, compared to 29.3 GW of cell manufacturing capacity and 120 GW of module manufacturing capacity. While India has achieved substantial growth in downstream manufacturing, the upstream segments that determine technological self-sufficiency and supply-chain resilience remain underdeveloped, leaving domestic producers heavily dependent on imported inputs.

A similar pattern is visible in critical minerals. Despite possessing the world’s third-largest rare earth reserves, estimated at 6.9 million tonnes according to the USGS Mineral Commodity Summaries 2025, India processes only a negligible share domestically. As a result, a substantial portion of the value chain continues to remain outside the country, even if end-use manufacturing has expanded.

The economic consequences of this dependence are highly visible. India’s solar sector imports during financial year 2024-25 totaled USD $7 billion, of which USD $3.89 billion originated in China. More importantly, recent export controls imposed by Beijing on heavy rare-earth elements and related magnets have demonstrated how concentrated supply chains can quickly become strategic vulnerabilities. This broader context is essential to understanding the significance of India’s March 2026 amendment.

The March 2026 Amendment: Recalibrating Supply-Chain Strategy

Recognizing the limits of a purely restrictive approach, the government recalibrated its supply‑chain strategy in March 2026 to prioritize capability building while allowing selective access to Chinese capital, technology, and expertise. The amendment uses two main mechanisms. First, it permits automatic‑route investments from non‑land‑bordering‑country entities with passive Chinese beneficial ownership up to 10 percent, addressing concerns from global institutional investors whose holdings had been unintentionally ensnared by PN3. Second, it mandates a statutory 60‑day approval window for direct investments originating from land‑bordering countries in seven strategically important sectors—capital goods, electronic capital goods, electronic components, polysilicon and ingot‑wafer manufacturing, advanced battery components, rare‑earth permanent magnets and rare‑earth processing—while retaining security reviews by relevant ministries and agencies.

A complementary regulatory move aims to translate renewed engagement into capacity building: On March 18, 2026, MNRE notified ALMM List‑III, requiring government‑backed solar projects to source domestically manufactured ingots and wafers from June 1, 2028. This will help ensure a robust future market for upstream producers. It also means that, for Chinese polysilicon and wafer firms facing domestic overcapacity and margin pressure, establishing local partnerships or joint ventures in India may be more attractive.

Politically, the amendment signals economic pragmatism rather than a diplomatic reset. Border disengagement in late 2024 and the resumption of flights in 2025 eased tensions, but the amendment appears driven more by industrial necessity still tempered by strategic caution.

Remaining Constraints: Why the Amendment Is Not a Complete Solution

The March 2026 amendment addresses important bottlenecks, but it does not eliminate the structural challenges facing India’s manufacturing ambitions. Three constraints in particular deserve attention.

The first concerns technology transfer. The assumption that Chinese investment will automatically accelerate domestic capability creation is not supported by historical experience. China’s rise in solar manufacturing was driven primarily by domestic scale, vertical integration, and sustained state support rather than by the overseas transfer of advanced production know-how. Even in countries such as Vietnam and Malaysia, where Chinese firms helped create substantial export-oriented solar manufacturing capacity, upstream polysilicon or wafer technology and expertise largely remained concentrated in China. Majority Indian ownership can ensure regulatory control, but it cannot compel the transfer of tacit manufacturing knowledge accumulated over decades. The more realistic near-term outcome is likely to be joint ventures, equipment partnerships, and localized manufacturing of selected production stages rather than a wholesale transfer of upstream technological capability. While limited, such arrangements could still represent a significant improvement over India’s current position.

Majority Indian ownership can ensure regulatory control, but it cannot compel the transfer of tacit manufacturing knowledge accumulated over decades.

The second challenge is commercial viability. Chinese dominance is also rooted in scale and state support. The Information Technology and Innovation Foundation (ITIF) notes that Chinese polysilicon producers have often expanded capacity despite operating at extremely low margins, or even losses, in pursuit of long-term market share. Organisation for Economic Co-operation and Development (OECD) analysis similarly highlights how sustained state support contributed to rapid capacity expansion and persistent oversupply, making it difficult for new entrants to compete. Under such conditions, access to foreign investment alone is unlikely to create a commercially viable upstream manufacturing ecosystem in India. Complementary measures—including dedicated polysilicon PLI, which is a topic under active discussion with the Ministry of Finance, long-term procurement commitments, and support for critical inputs—will be necessary if domestic manufacturing is to compete at scale.

The third challenge is strategic. The amendment seeks to reduce dependence on Chinese supply chains by selectively permitting greater Chinese participation in their development. While economically rational, this approach inevitably creates new forms of exposure. Future deterioration in bilateral relations could transform commercial linkages into sources of strategic vulnerability. Managing this risk requires diversification.

Encouragingly, India has begun pursuing such diversification in parallel. In February 2026, it joined Pax Silica, a U.S.-led twelve-country initiative to secure supply chains across AI, semiconductors, and critical minerals. In May 2026, India participated in the launch of the Quad Critical Minerals Initiative Framework, through which the Quad committed to mobilizing up to USD $20 billion in public and private investment for mining, processing, and recycling supply chains. These initiatives offer India an opportunity to build alternative supply-chain partnerships while continuing selective engagement with China.

India’s experience since 2020 suggests that supply-chain resilience cannot be achieved through restriction alone. The post-Galwan framework succeeded in constraining Chinese participation but did little to reduce dependence on Chinese technology, machinery and upstream industrial inputs. The March 2026 amendment reflects a growing recognition that industrial self-reliance ultimately depends on building domestic capability rather than simply limiting external engagement. For the foreseeable future, that task is likely to require a combination of selective cooperation with China and accelerated efforts to develop alternative supply-chain partnerships.

Views expressed are the author’s own and do not necessarily reflect the positions of South Asian Voices, the Stimson Center, or our supporters.

Also Read: The Limits of an India-China Détente

***

Image 1: Narendra Modi via X

Image 2: Wikimedia Commons